Seasonal small businesses can be a rewarding type of business to own and operate for those who enjoy extended periods of demanding work followed by an almost equal period of little work with time for more rest and recreation. There are over thirty-three million small businesses in the U.S. in 2023 and many of these small businesses are seasonal, especially those in retail and in e-commerce (U.S. Chamber of Commerce, 2025). A seasonal small business owner who also has another source of income would likely not be concerned with cash flow fluctuations inherent in seasonal businesses. Likewise, a seasonal small business owner who owned another business with the opposite season would likely not suffer from cash flow volatility, however, would forego enjoying a period of rest and rejuvenation enjoyed by the seasonal business owner with one business. For most seasonal small business owners though, the slow season brings to time of stretching the cash generated during the busy season to pay the fixed costs such as mortgages and utilities and taxes during the slow season (Zhua et al., 2023). Seasonal small businesses may suffer during their slow season unless they have saved cash generated during the busy season or have other resources to survive during their slow season. Alternatively, they may be using the cash generated in the busy season to make improvements and expansions while they have the cash, without regard to how much cash they will need to save for the slow season (Kamaliah et al., 2024). In addition, cash management during the busy season with a focus of saving for the slow season may be foregone as business owners are busy with day-to-day operations. Seasonal small businesses may also be affected by uncontrollable external factors such as the economy and weather more dramatically than small businesses that are not seasonal. Brown et al. (2021) found that severe weather does affect cash flows in businesses. Since a seasonal small business relies on most of its annual cash flow generation during its busy season, adverse weather during that time would affect both the cash inflows and outflows. For example, unusually cold temperatures or unusually long periods of rain would affect a summer seasonal business’s cash inflows due to lack of tourists (Shields & Shelleman, 2013) and may affect cash outflows with increased utility bills or rainwater mitigation costs. Seasonal small businesses must prepare for these possible weather-related cash flow interruptions in addition to the volatility of cash flows due to the inherent seasonality of the business. The purpose of this paper is to propose five strategies for seasonal small businesses to manage cash flows during their busy season to increase available cash during their slow season. Cash flow management requires planning (Shields & Shelleman, 2013) and discipline and commitment to a plan as well as flexibility to change the plans if they need to be adjusted. Managing cash effectively also requires financial discipline (Appuhami et al., 2024) which Brown et al. (2021) states is not an inherent trait among small business owners.

Financial Discipline

Financial discipline involves maintaining respect for keeping track of finances and building a positive attitude toward money in general (Kamaliah et al., 2024). Many seasonal small business owners do not enjoy the accounting aspects of keeping track of business, especially during the busy season when time must be focused on the operations. Financial discipline requires some degree of financial literacy. Financial literacy is the ability to understand the implications of financial decisions through knowing how to read financial reports, understanding the risks involved with borrowing and capital spending, and exercising financial discipline habits (Kristanto, 2022). Lack of financial literacy can undermine financial discipline and become a reason the business fails. The seasonal small business owner’s attitudes about financial discipline or aversion to accounting and financial administrative tasks may negatively influence their cash flow management strategies (Kristanto, 2022).

Empirical studies show that financial literacy in small business owners is relatively low. Eniola and Entebank (2017) claim the lack of financial literacy is a common problem for small businesses. Smit and Kotzè (2008) show that a lack of financial literacy is a major reason for small business failure. On the other hand, Widdowson and Hailwood (2007) found that financial literacy helps small business owners succeed. The authors found that when small business owners take advantage of increasing competition in financial markets by applying risk management knowledge and financial literacy skills enabling them to communicate more effectively with bankers, their business is more successful. According to Kristanto (2022) small businesses need financial literacy to make good financial decisions. Kristanto also found that financial education helps small business owners to overcome challenges in obtaining loans and managing cash reserves. Financial discipline, supported by financial literacy, is a successful combination for all small business owners and especially for those who own seasonal businesses with cash flow challenges. In addition, financial literacy will enhance obtaining loans and lines of credit (Kristanto, 2022) while financial discipline may help small business owners manage their cash flows successfully (Przychocka et al., 2024).

Small Business Seasonality

Shields and Shelleman (2013) studied small business seasonality by surveying 73 small business owners and gathering data on the cyclical demand attributes and seasonality phases of small businesses. The authors found four phases of seasonality: Shoulder up, busy, shoulder down, and slow, with each season having a duration of one to three and a half months depending on the type of business. They also found that seasons are affected by weather, regular customers vacationing, holiday weekends, and school year cycles. The authors studied the ways in which the seasonal business owners managed tasks according to the seasons. For example, they found that the owners in their study saved cash generated in the busy season for use in the slow season as their most mentioned task in the busy season. Other tasks related to cash management undertaken during the busy season mentioned in the study included hiring additional employees and increasing prices. During the shouldering down season most tasks were related to cash management such as decreasing employee hours, discounting prices, decreasing advertising, and decreasing inventory purchases. The slow season cash management related activities included retaining critical employees. According to Shields and Shelleman (2013) very few of the owners in their study closed down for the slow season. The shouldering up season cash management related tasks were similar to shouldering down, but in the opposite direction.

Small Business Cash Flow Management in Adverse Conditions

Small businesses are more vulnerable to uncertainties caused by weather, economic factors, and political factors more significantly than large businesses (Przychocka et al., 2024). Wiatt et al. (2021) studied small business recovery after a natural disaster. The authors surveyed 499 small businesses in Southern Mississippi several years after Hurricane Katrina. The businesses surveyed reported frequent shortfalls in cash that were satisfied by the use of family resources and utilizing alternative financing strategies such as bootstrapping. According to Wiatt et al. (2021) bootstrapping, which is using methods of obtaining resources other than through financial institutions, occurs often in small businesses. The authors found that financial recovery occurs in the short term after a natural disaster and financial resilience is the long-term ways in which operations are conducted after recovery. Resilience includes reorganizing the business after the disaster while recovery is achieved by opening as quickly as possible after the disaster. The authors also found that businesses that had employees survived more often than businesses with no employees. Implications of the study indicate that small business owners should be educated on cash flow management and bootstrapping as a form of maintaining positive cash flow (Wiatt et al., 2021).

According to Przychocka et al. (2024) small businesses must approach planning for uncertainties seriously and systematically using modern tools such as financial management software, data analytics, and e-commerce platforms to build financial resilience. The authors studied European small businesses in the wake of the Russian invasion of Ukraine in 2022 and inflation that occurred due to changes in global markets. The authors recommend that small businesses regularly forecast and manage cash flow gaps to maintain liquidity. Identifying potential risks of reduced cash inflows and increased cash outflows is also a strategy the authors recommend.

Olubimbo and Omotayo (2021) studied how small construction companies manage their cash flows to remain financially stable. The small and micro businesses the authors surveyed had remained in business for ten years or more. The authors found several strategies these construction businesses employed to manage cash flows. The businesses surveyed used favorable trade credit with suppliers to delay payments and also structured their client billing with front-loading which allowed them to receive more cash at the beginning of the project. The most practiced technique for cash flow management in the study was to structure bids for projects with low profit margins to increase the probability they would win the contract. The authors’ recommendations from the findings suggest that the use of favorable trade credit terms should be maximized as the most favorable cash flow management technique. The practice of low profit margin bidding increases the volume of contracts but does not guarantee to contribute to cash inflows in proportion. In addition, the practice of front-loading may have ethical implications and compliance issues with accounting standards.

Strategies for Managing Cash Flow in a Seasonal Business

This paper proposes five strategies to manage cash flow in a seasonal small business. Each seasonal small business has unique circumstances however these strategies may provide ways in which successful seasonal cash management may be achieved in many types of seasonal businesses and economic environments. The strategies presented are not presented in ranked order but could be implemented in the order presented. The least difficult strategy to implement is presented first and the most difficult strategy to implement presented last. Employing the four seasons Shields and Shelleman (2013) found in their study, the strategies proposed in this paper will indicate if implementation would be best during the shoulder up phase, the busy phase, the shoulder down phase, or the slow phase.

Strategy 1: Maintain a Weekly Cash Flow Budget

Uhlig et al. (2023) found that planning behaviors undertaken at the beginning of the week positively benefited overall work engagement and completing unfinished tasks at the end of the week. Maintaining a weekly cash flow budget is an effective way to understand a business’s cash inflows and outflows and provides information for decision making (Przychocka et al., 2024). Seasonal small business owners may experience difficulty managing time to maintain the weekly cash flow projections during the busy season as they focus on operations (Hidayati et al., 2023). This strategy of maintaining a weekly cash flow budget may be implemented anytime and maintained weekly during all four seasons. The weekly cash flow budget can aid small business owners in learning the cash flow patterns of their business and provide better planning and decision-making in every season. Figure 1 in the Appendix provides an example of a weekly cash flow budget forecast in Excel based on common costs in small business.

Strategy 2: Maintain Boundaries with Family and Employee Requests for Cash

When plenty of cash is available, it may be more difficult for the small business owner to resist generous gifts to family and good employees by providing bonuses and raises. The shouldering down season brings a time when cash may still be plentiful if the season was successful (Shields & Shelleman, 2013), and the slow season may not seem so daunting. Seasonal small business owners that implement the first proposed strategy of maintaining a weekly cash flow budget may use this budget to support decisions for cash advancements to family or employees. The savings section of the budget shows the amount of cash on-hand to pay fixed costs not covered by slow season cash inflows. Figure 1 in the Appendix shows the example of cash savings where the decision may be made to use excess cash for expansion or investments or to gift to family and employees. Figure 2 in the Appendix shows an example of how the weekly cash flows budget may be used in the shouldering down season to support cash outflow decisions by adding the number of weeks remaining until the next busy season and determining how much excess cash per week is available during the shouldering down, slow, and shouldering up seasons.

Strategy 3: Temporary Funding Pays Bills, Not Expansion Projects

The slow season for a seasonal business may be a time when expansion projects may be initiated. The slow season may also be a time when cash on hand is low and meeting the fixed costs such as mortgages and utilities that continue through the slow season may be challenging (Shields & Shelleman, 2013). Seasonal small business owners may bootstrap or use credit cards during the shouldering up season to stretch to the busy season when these costs will be covered by the excess cash flows in the busy season. Credit card use should be considered as working capital, or short-term debt (Harvard University Clinics, 2015). Expansion projects may facilitate creating more volume in the next busy season, but the cost of the expansion, or capital needed for the expansion, should be funded with long-term payback in mind while cash needed for current bills should be funded with short-term, or working capital, payback in mind. Credit lines are another form of borrowing that may be available to seasonal small business owners. According to Brown et al. (2021) bank credit lines are an important tool for managing cash flow volatility in small businesses, especially if the small business is solvent and the bank from which the small business is borrowing is a local bank.

Budgeting for capital projects requires careful planning with cash flows discounted to determine the present value of the cash flows meets or exceeds the invested amount. Seasonal small businesses carry more risk with endeavors that require a new fixed cost payment (Kristanto, 2022). Risk associated with implementing an expansion project may be determined by understanding the seasonal business’s regular cash flows during the busy season and the difference in cash flows in the slow season. According to Kristanto (2022) seasonal small business owners need financial literacy to assess risk to make sound decisions about long-term financing. Figure 3 in the Appendix illustrates a cash flow budget with an added capital expenditures section.

Strategy 4: Apply Due Diligence When Seeking Funding

If external funding is needed during the slow season, due diligence must be applied to determine the type of funding to obtain. External funding for paying existing fixed costs should be short-term financing to match the short-term nature of existing costs (Kristanto, 2022). Long-term loans obtained for large projects may require external funding such as bank loans. The most common forms of small business capital funding include friends and family support, bank loans (traditional loans, home equity loans, and credit lines), government supported loans such as from the Small Business Administration, and fundraising through crowdfunding (Harvard University Clinics, 2015). Table 1 below provides guidelines for choosing potential long-term project funding strategies.

Table 1 shows that seasonal small business owners seeking funding to pay existing fixed costs during slow season and shouldering up season, for example under $50,000, may use savings, credit cards, and even crowdfunding campaigns. For larger projects over $50,000 loans and investors may be needed to provide capital.

Strategy 5: Cost-Volume-Profit Analysis for Planning and Forecasting

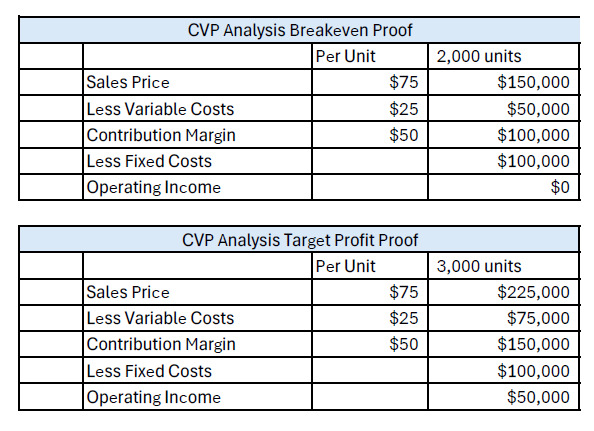

Seasonal small business owners have accepted the risks associated with operating a seasonal business and after two to three years of owning and operating a seasonal small business will likely have a good understanding of their seasonal cash inflows, (Shields & Shelleman, 2013). At the beginning of a new busy season, the pricing of the product or service may need to increase, factors may cause sales volume to increase or decrease, and variable costs to purchase or make products or provide services could increase. Any of these changes will affect cash flows and can be anticipated or leveraged to optimize profits in accordance with the changes. Cost-Volume-Profit (CVP) analysis techniques provide information for forecasting and planning for changes in costs and how those changes will relate to volume and profit. According to Hidayati et al. (2023) small businesses tend to focus operations on surviving. However, Shields and Shelleman (2013) found that seasonal small business owners in their study used the slow season for planning. CVP analysis is a tool that can be used for planning, growth, and profit optimization (Hidayati et al., 2023). CVP analysis techniques include calculating breakeven, target profit, and multiple scenarios of sales volume and sales prices. A caveat with CVP analysis is the assumptions made when forecasting pricing and volume. Viewing CVP results as an estimate can be useful for providing information for decision making. For example, some seasonal small business owners raise prices during busy season (Shields & Shelleman, 2013). CVP analysis may be used to forecast the achievement of the desired profit given the new pricing. Similarly, small business owners may experience an increase in their inventory costs during the busy season. CVP analysis may be used to forecast the impact of the increase in the inventory cost to determine at what point profit will be achieved. Figure 4 in the Appendix illustrates target profit and breakeven through the variable costing income statement where inventory is considered a variable cost.

Implementing the Proposed Cash Flow Strategies for Seasonal Small Businesses

The five proposed cash flow strategies for seasonal small business owners are summarized below in Table 2 with the suggested season in which implementation of the strategy may best occur.

Recommendations for Future Research and Conclusion

Seasonal small businesses can provide distinctive periods of time with different objectives for the owners to address. Managing cash flows during the shouldering down season through the shouldering up season can be challenging if the owner has not planned properly to save or invest cash generated during the busy season for use during the slower seasons. The five strategies proposed in this paper are supported by the literature on financial discipline, small business seasonality, and small business cash flow management. Financial discipline is a key indicator of success in small business (Kamaliah et al., 2024). One key discipline seasonal small business owners can employ is saving cash generated during the busy season for use in the slow season (Shields & Shelleman, 2013). Cash flow management can be enhanced with the use of tools such as financial tracking software (Przychocka et al., 2024) and cash flow budgets prepared with Excel spreadsheets as presented in Appendix A.

Further research in specific industries could provide more specific strategies for seasonal businesses in that industry. Other studies involving interviews with seasonal small business owners would likely garner new and fresh insights and updated strategies for cash flow management within each season. Many small businesses not considered seasonal have a seasonal component such as construction businesses and could also benefit from strategies proposed in this paper. Small business advisors may also find the strategies proposed in this paper useful for their clients’ success. Cash flow management for any small business can become an important issue in times of uncertainty. This paper proposes that by focusing on strategies based on financial discipline and financial literacy, seasonal small businesses can enjoy each season of the year.